The financial industry is undergoing an AI evolution. Review our vision for Artificial Neural Networks (ANN) and deep learning targeted for banking, check payments, and fraud detection.

Sign up for quarterly meeting -- content includes best practices, fraud cases, and trends (for financial institutions)

AI and Deep Learning-Based Check Recognition

Check recognition is the most important component in today's check processing and omni-channel capture. Learn how OrboAnywhere using OrbNet AI technology reduces costs and mitigates risk for any check image capture workflow.

An informative blog series exploring checks, payments, and banking technology and innovation

About Us

Celebrating over 30 years of innovation, OrboGraph has transformed into an AI company delivering targeted fraud prevention and automation solutions to the banking and payments industry.

Reach out if you have a specific request and would like an OrboGraph representative to contact you.

Social Media

Resources

From news and events to case studies, trends, and videos, this section provides a range of informational resources for payment automation, fraud detection, and innovations in payments.

Experience the excitement of previous tech conferences through pictures and video

Blogs

OrboGraph is now publishing several blog series on a weekly basis, covering topics from check processing, fraud prevention, and AI technology. We hope you enjoy the content!

Blog commentary, published weekly, addressing today's hottest topics in payments and check fraud. We analyze industry publications, new technologies, video reports, and an array of fraud perspectives

Join the OrboNation Payments movement as we explore the payments industry with varying perspectives of electronic, paper, fraud, AI, and other intriguing topics involving the movement of money

Upgrade IQA capabilities, mitigate risk by validating payment negotiability, and enhance deposit review

Solution Overview

Anywhere Validate automatically validates the negotiability of paper-originated items for any self-service, centralized or distributed capture channel or image exchange trading partner within the omnichannel of a financial institution. Designed to minimize the risk of checks and cash equivalent images from being non-negotiable, the system is a more comprehensive approach compared to traditional image quality, image usability, and/or manual review processes. In many cases, Anywhere Validate can eliminate the manual functions of what a teller performs on deposited items.

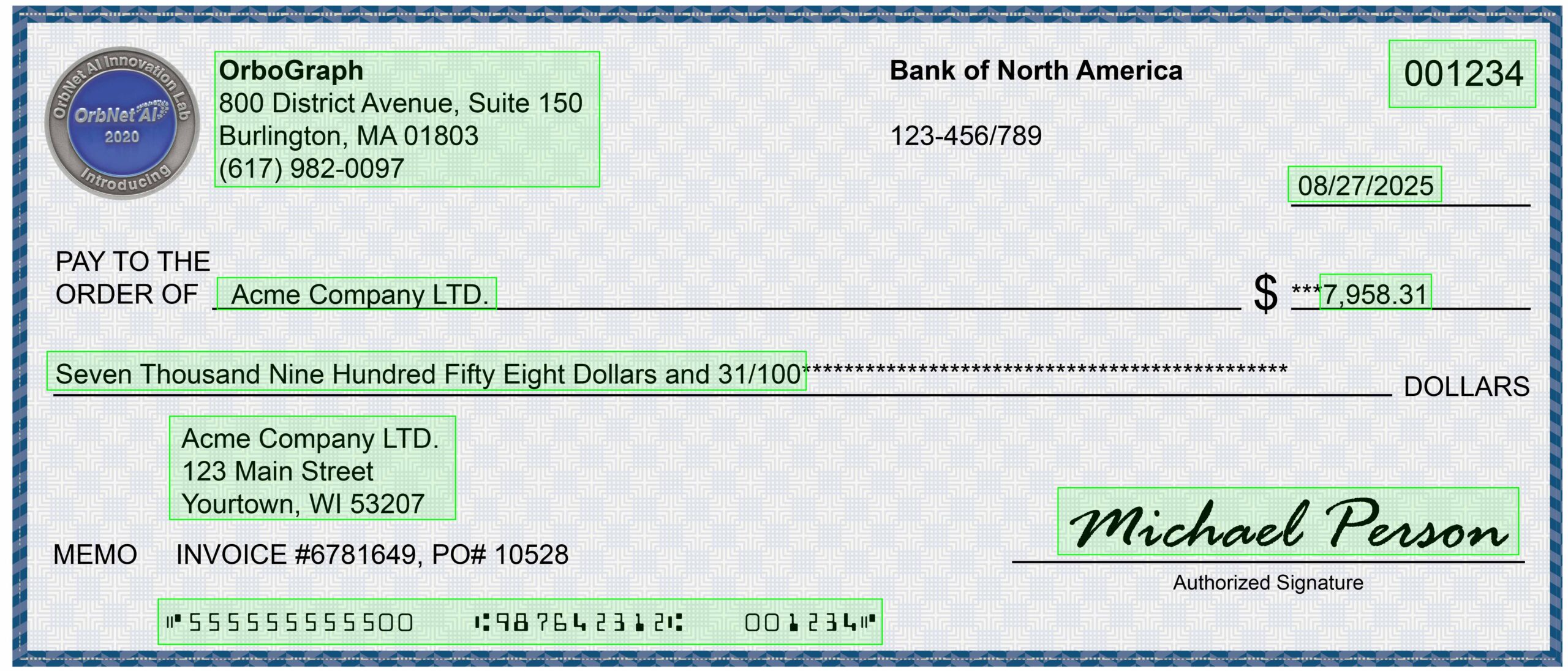

Anywhere Validate applies OrbNet AI recognition to the following fields:

Field

Description

CAR

Courtesy amount used for posting

LAR

Legal amount used for posting and comparison to CAR

Amount

Net of check used in posting

MICR

MICR line used for reject correction, free read of non-MICR items

Payee

Matches to payee name data generated from Anywhere Payee

Payer

Payer data (Parsed fields) Free read used for kiting analysis, risk per channel, downstream data analysis, and marketing campaigns targeting payors from transit banks

Signature

Identify customer errors, limit operational errors, ensure LAR precedence

Document

Document IQA: Tests 13 variations of quality analyzers

Date

Date used for post/stale date detection and fraud

Serial

Check serial number reads supplement MICR correction and fraud

Rear Endorsement

Rear endorsement existence confirms endorsement presence

A negotiable instrument is a written document that guarantees the payment of a specific amount of money, either on demand or at a set time, and is transferable from one person to another. Common examples include checks, promissory notes, and drafts. The key feature of a negotiable instrument is its ability to be endorsed and transferred, allowing the holder in due course to claim payment in good faith without concern for the original transaction. Governed by the Uniform Commercial Code (UCC) in the United States, negotiable instruments play a vital role in facilitating commerce and credit by providing a secure and efficient means of payment and transfer of funds.

Payment negotiability refers to the ability of a financial instrument—such as a check, promissory note, or draft—to be freely transferred or assigned from one party to another, giving the new holder the right to receive payment. This concept ensures that the instrument functions much like cash, allowing it to circulate easily within the financial system. For an instrument to be negotiable, it must meet specific legal requirements, such as being in writing, signed by the issuer, containing an unconditional promise or order to pay a fixed amount, and being payable either on demand or at a definite time. Payment negotiability is fundamental to modern commerce, as it promotes liquidity, trust, and efficiency in financial transactions.

From these recognition field results, 25+ validation tests are activated to protect all potential parties within the payment stream including:

Bank of first deposit (BOFD)

Paying bank

Retail customer

Corporate client

Each validation test, activated in either real-time or batch, creates a document negotiability score. This output overall analysis approach from big data/analytics/capture/fraud systems, streamlining traditional check deposit review functions.

Current Tests Performed by Anywhere Validate:

Field/Type

Name

Use Cases and Tangible Achievements

Document

Image Quality Assurance (IQA)

16 IQA tests that minimize non-compliant images (NCI) and identifies quality issues, classifies document type for downstream processing and reporting.

Document

Illegal Document Identification

Identifies RCC/PAD items per ECCHO rules, validates approved document types as defined in bank customer relationships on a workflow level, i.e. RDC, ATM.

Document

Doc Type ID

Validates Appropriate Document Type.

Document

Cash Equivalent

Detects items considered same day or day 1 funds availability, See Anywhere Compliance for more details.

Amount

High Dollar Threshold

Risk management for manual review, internal controls, SAR reporting.

Amount

Verification (CAR, LAR, Index compare)

UDAAP & Reg CC risk mitigation, minimize customer errors, limit cash letter errors, reduce adjustments. AV previously known in the industry as amount encode verification (AEV), now delivers 99%+ coverage of items.. Incorrect inclearing amounts can range from 10 to as high as 50 per 100K items.

Amount

Discrepancy (CAR vs. LAR)

Identify customer errors, limit operational errors, ensure LAR precedence in deposits.

Date

Stale and Post Date

Risk and fraud related topic, UCC related topic, date ranges are flexible per workflow.

Depositor

Check Out of State

Identify payors from outside of state which may pose risk, international items, feeds downstream data analysis.

Endorsement

Presence Detection

Identifies that a signature is present on image.

MICR

Image Integrity

Compares the MICR line via recognition to the index/metadata values to identify incorrect images associated with MICR.

Payee

Cash Detector

Flag items payable to “CASH”.

Payee

Account Name Comparison

Compare payee against account holder name. Flag if they do not match.

Payee/Payor

Field Comparison

Flag is the check maker (payor) matches the payee.

Payor

Suspicious Payor

Flag if the payor information on the check is suspicious.

Payor

Check Out of State

Flag if the state of the payor on the face of the check is different from the state of the deposit address.

Payor

Account Name Comparison

Compare payor against account holder name. Flag if they do not match.

Payor

Negative List

Identify payors/makers from predetermined lists, i.e. black list, closed accounts, fraud, other.

Payor

Deposit Out of State

Flag if the state of the account holder address is different from the state of the deposit address, risk indicator, risk mitigation of suspect customers, KYC.

Signature

Presence Detection

Reg CC, UCC and ECCHO rule compliance to confirm signature is on image.

Signature

PAD Detection

Flag an item which has been detected as PAD.

Transaction

Account Negative List

Flag if the payor account (MICR) on the check matches information in a negative account list.

Transaction

New Account Identification

Identified via application API, fraud and risk control, funds availability considerations, manual review queues.

Transaction

Short Term Duplicate

Flags immediate duplicates where customer or application submits images more than once.

Contact OrboGraph to perform an analysis on your images for non-negotiable items or to identify incorrect amounts on your inclearing items.

Want to learn more?

Request Additional Information

Complete the form below to receive additional information.

data, information, automation, insurance, regulatory compliance, data integrity, risk, workflow, artificial intelligence, database, data management, machine learning, know your customer, analytics, onboarding, payment, efficiency, technology, behavior, customer experience, audit, software, user interface, data validation, check processing, detect fraud, validation tools, fraud detection, automated validation, data quality, learning, intelligence, data analysis, deep learning, quality management, customer, operational efficiency, marketing, financial institution, optical character recognition, confidence, document, productivity, risk assessment, invoice, user experience, organization, governance, identity fraud, data set, recognition, check, account, automated, accounts, ach, checks, compliance, verification, bank account, fraud, ownership, credit card, api, automated clearing house, nacha, services, payee, businesses, identity, account verification, loan, encryption, risk management, management, debt, fee, authentication, reputation, data sources, verify, vendors, global, validation services, bank account validation, account validation, bank account verification, sources, due diligence, financial crime, web portal, friction, software system, software engineering, system, computer programming, specification, software quality, software bug, software testing, software development, traceability, project management, software verification and validation, requirement, test automation, test case, mobile banking, regression testing, verification and validation, quality assurance, functional testing, devops, software project management, configuration management, software verification, software requirements, usability, usability testing, user, software maintenance, software development process, reliability engineering, engineer, rapid application development, agile software development, end user, acceptance testing, code review, inspection, system testing, test plan, unit testing, interface, medical device, formal verification, validation test, user acceptance testing, software validation, test management, test cases, best email validation tool, scope, experience, concept, methodology, waterfall model, stakeholder, prototype, software design, simulation, quality control, black box, architecture, integral, traceability matrix, matrix, capability maturity model, regulation, mobile app, source code, jira, pdf, requirements traceability, software architecture, data model, spiral model, complexity, software product, validation process, development, software development lifecycle, quality, read, validation testing, email validation tools, free email validator, email address verification tool, email verify tool, bulk email checker free, free email verify, email address validation tool, free email address validator, free email validator online

Frequently Asked Questions

How does the Anywhere Validate solution work?

The Anywhere Validate solution works by utilizing advanced AI recognition technologies to analyze and validate financial payment documents in real-time, ensuring accurate identification of misencoded items and confirming payment negotiability.

What are the key benefits of using payment validation services?

The key benefits of using payment validation services include enhanced accuracy in identifying misencoded items, improved fraud detection, and increased payment negotiability, ultimately leading to greater operational efficiency and reduced financial risk for businesses in the financial industry.

How can automated check validation systems improve fraud detection?

Automated check validation systems enhance fraud detection by utilizing advanced algorithms to analyze transaction patterns, identify anomalies, and verify authenticity in real-time, significantly reducing the risk of fraudulent activities in financial transactions.

What features does OrboGraphs Anywhere Validate service offer?

The features of OrboGraph's Anywhere Validate service include real-time payment validation, advanced misencoding detection, and comprehensive testing for payment negotiability, all powered by cutting-edge AI technology to enhance fraud prevention in the financial sector.

How does AI enhance payment validation processes?

AI enhances payment validation processes by utilizing advanced algorithms to quickly identify misencoded items and assess payment negotiability, thereby streamlining fraud detection and ensuring accurate transaction processing in real-time.

What technology powers the Anywhere Validate solution?

The technology that powers the Anywhere Validate solution includes advanced AI algorithms and recognition technologies that facilitate real-time validation of financial payments, ensuring accurate identification of misencoded items and enhancing fraud detection capabilities.

How does Anywhere Validate ensure payment accuracy?

Anywhere Validate ensures payment accuracy by utilizing advanced recognition technologies to verify misencoded items and assess payment negotiability in real-time, significantly reducing errors and enhancing fraud detection in financial transactions.

What industries benefit from payment validation services?

Various industries benefit from payment validation services, particularly the financial sector, retail, e-commerce, and healthcare. These services enhance transaction accuracy, reduce fraud, and ensure compliance, ultimately safeguarding financial operations across these sectors.

How can payment validation reduce fraud risks?

Payment validation reduces fraud risks by ensuring the accuracy and legitimacy of financial transactions. By identifying misencoded items and verifying payment negotiability in real-time, it helps prevent unauthorized payments and enhances overall security in the payment process.

What is the process for validating checks?

The process for validating checks involves verifying the accuracy of the check's information, ensuring it meets payment negotiability standards, and using advanced recognition technologies to detect any discrepancies or potential fraud in real-time.

How does AI improve payment processing efficiency?

AI improves payment processing efficiency by automating transaction validation, reducing manual errors, and accelerating decision-making. This leads to faster processing times, enhanced accuracy, and improved fraud detection, ultimately streamlining financial operations for businesses.

What are the limitations of check validation software?

The limitations of check validation software include potential inaccuracies in recognizing misencoded items, reliance on high-quality images, and challenges in adapting to evolving fraud techniques, which may hinder its effectiveness in real-time payment validation.

How does automated validation enhance transaction security?

Automated validation enhances transaction security by utilizing advanced recognition technologies to detect anomalies and misencoded items in real-time, ensuring that only legitimate transactions are processed and significantly reducing the risk of fraud.

What metrics measure the effectiveness of payment validation?

The metrics that measure the effectiveness of payment validation include accuracy rates, false positive and negative rates, processing speed, and the volume of validated transactions, which collectively assess the solution's reliability and efficiency in preventing fraud.

How frequently should payment validation be performed?

Payment validation should be performed regularly to ensure accuracy and prevent fraud. Ideally, it should occur in real-time during transaction processing and be supplemented with periodic audits to maintain ongoing compliance and security.

What challenges exist in payment validation systems?

The challenges that exist in payment validation systems include handling misencoded items, ensuring real-time processing, adapting to evolving fraud tactics, and maintaining compliance with regulatory standards. These factors can complicate the accuracy and efficiency of payment validation.

How does Anywhere Validate handle misencoded items?

Anywhere Validate effectively identifies and corrects misencoded items by utilizing advanced recognition technologies. This ensures accurate payment validation and enhances fraud detection, maintaining the integrity of financial transactions in real-time.

What role does machine learning play in validation?

The role of machine learning in validation is crucial, as it enhances accuracy by analyzing large datasets to identify patterns and anomalies, ensuring reliable payment validation and effective fraud detection in real-time.

How can businesses implement payment validation solutions?

Businesses can implement payment validation solutions by integrating AI-powered technologies that analyze transaction data in real-time, ensuring accurate payment processing and enhancing fraud detection capabilities. This involves selecting a reliable service provider and customizing the solution to meet specific operational needs.

What are the costs associated with validation services?

The costs associated with validation services vary based on the specific solution and volume of transactions. For detailed pricing, please contact OrboGraph to discuss your needs and receive a tailored quote.

How does real-time validation impact customer experience?

Real-time validation significantly enhances customer experience by ensuring immediate feedback on payment negotiability, reducing transaction errors, and minimizing delays. This leads to smoother transactions, increased trust, and overall satisfaction in financial interactions.

What are common errors in check processing?

Common errors in check processing include misencoded amounts, incorrect payee names, and illegible handwriting. These mistakes can lead to payment delays and increased risk of fraud, highlighting the need for robust validation solutions.

How can validation services improve cash flow?

Validation services enhance cash flow by ensuring accurate processing of payments, reducing errors and disputes, and accelerating transaction approvals. This efficiency minimizes delays, allowing businesses to receive funds faster and maintain healthier cash flow management.

What features differentiate OrboGraphs solution from competitors?

The features that differentiate OrboGraph's solution from competitors include advanced AI-driven recognition technologies, real-time payment validation capabilities, and a strong focus on ensuring payment negotiability and fraud prevention.

How does Anywhere Validate integrate with existing systems?

Anywhere Validate integrates seamlessly with existing systems by utilizing APIs and customizable interfaces, ensuring smooth data exchange and enhancing payment validation processes without disrupting current workflows.

What training is required for using validation software?

The training required for using validation software typically includes understanding the software's interface, learning how to configure settings for payment validation, and familiarizing oneself with the specific fraud detection features it offers.

How can users access Anywhere Validates features?

Users can access Anywhere Validate's features through our user-friendly platform, which integrates seamlessly with existing financial systems, allowing for real-time payment validation and fraud detection capabilities.

What support options are available for validation services?

The support options available for validation services include comprehensive technical assistance, user guides, and dedicated customer service to ensure seamless implementation and operation of our solutions.

How does the solution adapt to new fraud tactics?

The solution adapts to new fraud tactics by continuously learning from emerging patterns and leveraging AI technologies to enhance its detection algorithms, ensuring real-time updates and improved accuracy in identifying fraudulent activities.

What feedback do users provide about Anywhere Validate?

User feedback about Anywhere Validate highlights its accuracy in identifying misencoded items and its efficiency in validating payment negotiability, with many praising its real-time capabilities and significant impact on fraud prevention.