Stolen Check Prices Drop on the Dark Web — What It Means for Financial Institutions

- The value of stolen checks in the "black market" has gone down substantially

- This is due to a massive "oversupply" of available stolen checks

- Plummeting prices may also be a result of lower ROI on stolen checks

Just a few years ago, stolen checks were considered premium commodities in the criminal underworld. As noted in previous posts, stolen checks routinely end up on the "dark web" or Telegram, creating a flourishing fraud market. Back in 2023, criminals could purchase a single personal check for $150 and business checks could fetch $250.

Things have changed over the past two years. David Maimon points out the price of stolen checks sold on the Telegram "black market" has dropped dramatically:

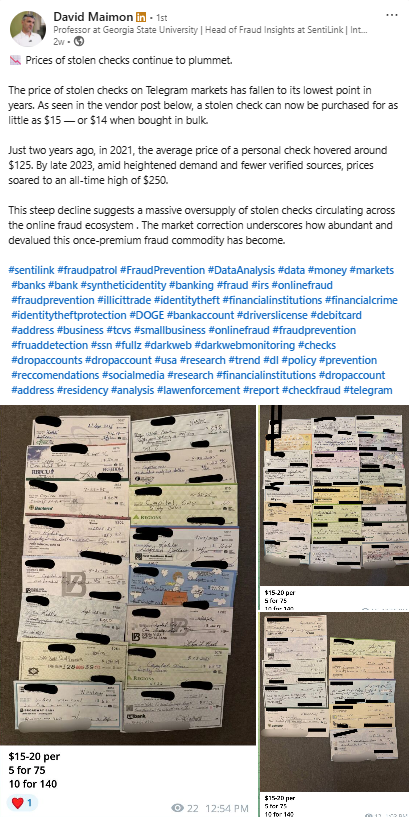

The price of stolen checks on Telegram markets has fallen to its lowest point in years. As seen in the vendor post below, a stolen check can now be purchased for as little as $15 — or $14 when bought in bulk.

[click to enlarge]

Lower Prices = Higher Levels of Mail Theft

The current steep decline in value suggests a massive oversupply of stolen checks circulating across the online fraud ecosystem -- a once-premium fraud commodity has become abundant and devalued.

Frank Albergo, National President of the Postal Police Officers Association, commented:

[Source: Frank Albergo LinkedIn]

Put bluntly: criminals can now acquire large volumes of stolen checks for pocket change because those checks are being taken en masse — from cluster boxes, collection boxes, and other soft USPS targets — with minimal detection.

That oversupply has real consequences. It turned what used to be a relatively rare crime into an industrialized pipeline. It also makes traditional investigative responses less effective — one arrest doesn’t dent a market flooded by thousands of easily stolen items.

This is, of course, bad news for financial institutions for the following reasons:

- Oversupply Equals Industrialized Fraud: The new lower prices signal a massive oversupply of stolen checks -- criminals are able to steal large volumes of checks easily, often from vulnerable USPS mailboxes. The new abundance of cheap stolen checks means fraudsters can operate on a much larger, more industrial scale.

- Lower Risk and Higher Volume for Criminals: When a stolen check costs pocket change, it becomes easy for fraudsters to purchase them in bulk, which lowers their risk and cost per transaction. It only takes a few successful fraudulent deposits for criminals to make a significant profit, even if most attempts fail.

- Traditional Law Enforcement Isn’t Keeping Up: As thousands of stolen checks flood the market, an occasional investigation or arrest does little to dent the supply. The sheer availability makes preventive measures and traditional bank antifraud responses less effective.

- More Consumer and Operational Risk for Banks: Banks face higher exposure to losses, operational headaches, and reputational damage as fraudulent check deposits rise.

Or -- Could Financial Institutions be Catching Up?

In the comment section of Dr. Maimon's LinkedIn post, Featurespace's VP of Delivery Majid Malek provides an interesting perspective:

It is also possible that the plummeting price is a result of lower ROI on stolen checks because fraud systems are improving. I’m sure both are happening (oversupply and improved defenses).

More financial institutions have adopted check fraud detection technologies like image forensic AI which effectively reduce the success rate for fraudster. This, in turn, may have turned a portion of the fraudsters away from check fraud. But, as we noted in a post earlier this week:

Each individual bank -- even each individual branch -- had a unique experience. As we've noted previously, check fraud appears to be regional, meaning that all banks did not feel the same urgency to adopt the latest check fraud detection technologies, so we cannot assume widespread adoption. In fact, the demand for check fraud detection technologies is still booming today -- from large financial institutions to community banks. And, it's not because these financial institutions are looking to get "ahead of the curve."

Unfortunately, there is not enough data for a concrete conclusion. However, financial institutions should be aware that the dangers of check fraud are more evident than ever.