Financial Crimes: FIs Need to Improve Fraud & AML Response Times

- The US accounts for a huge percentage of global money laundering

- Online check fraud communities have contributed

- A very large percentage of money laundering cases go undetected

Financial crimes encompass all payment channels for financial institutions. Unfortunately, many FIs still continue to silo different facets, including AML and check fraud. While this separation enables operations to concentrate internal resources to specific purposes, it also leads to less-effective fraud strategy.

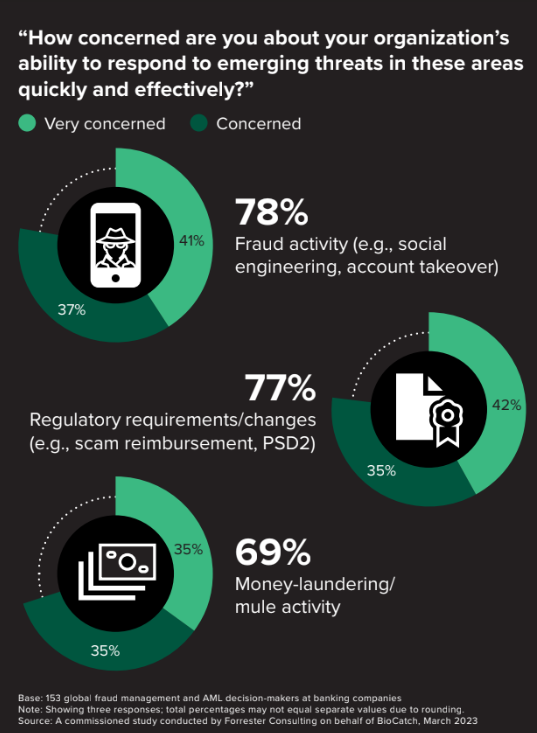

As we noted in an earlier post, there was a 50% increase in AML fines levied in 2022. According an article posted on Tearsheet, the US owns a significant portion:

Money laundering in the US makes up 15% to 35% of all money laundering in the world. Around $800 billion to $2 trillion is laundered globally and $300 billion of that amount is laundered in the US.

On top of the increase in money-laundering, FIs are faced with the resurgence of check fraud, aided by online "fraud shop" communities like Telegram:

Q6 Cyber found at least 30 channels on Telegram which curated the latest tips and tricks that enabled bank fraud. The biggest of these groups had 20,000 members. In 2022, the number of Suspicious Activity Reports (SARs) related to check fraud reached over 680,000, according to FinCen.

Slow Response Time Causing Issues

The Q6 Cyber report also pointed out that quick response to money laundering and check fraud is essential.

However...

69% of organizations report experiencing an increase in the number of days spent on investigations. And each day comes at a price, with 75% reporting that each additional day poses more financial risk to their organization.

With costs and financial risk increasing with time, early detection can significantly improve matters, however 60% of officials report that their firm has trouble responding to instances of crime early.

The report points to the separation between Anti-Money Laundering units and Enterprise Fraud Management units as one particularly problematic area:

Source: Tearsheet

Click the image above to enlarge

....Despite the two having significant overlap in the data they use and their objectives. This separation can lead to added cost and time and limits visibility and information sharing. Integration of these two functions across the people, processes, and tools used can considerably increase the efficacy of fighting fraud. Only one-third of organizations say they have full integration across both teams, though.

Another perplexing statistic from the Q6 Cyber report: Despite the fact that 91.1% of money laundering offenders are imprisoned, 90% of money laundering crimes go undetected.

Technology to Reduce Response Time

In ordering to effectively reduce response times, FIs need to evaluate their current operational structure and break down the silos between fraud groups. Instead of sharing data between two or more silos, having a singular department or group that can amalgamate all financial crime data will produce better results -- from increased detection to lower response time.

Additionally, the utilization of artificial intelligence and deep learning technologies will be key for AML and fraud detection -- including checks. FIs can leverage behavioral analytics to monitor accounts and transactions, while simultaneously running image forensic AI to analyze check images. When you complement these with other technologies such as dark web monitoring and consortium data, the fraud department/group now has a plethora of data to identify fraudulent activities -- all within seconds of when the transaction or activity was performed.

FIs that are focusing on breaking down barriers and taking a proactive approach to financial crimes will undoubtedly fare better than those who continue to operate as is.