Customer Acquisition

Congress passed a $2 trillion stimulus bill — the largest in United States history — that promises to revive a coronavirus-stricken economy. These are payments that will be sent directly to Americans, with many adults getting $1,200. For every qualifying child age 16 or under, the payment adds an additional $500. The plan is for…

Read More

MIT Sloan Management Review and Boston Consulting Group recently collaborated on a white paper exploring AI as a tool entitled Winning With AI (you can download the paper HERE). Subtitled Pioneers Combine Strategy, Organizational Behavior, and Technology, the white paper is a nice encapsulation of their global survey. Conducted in Spring 2019, the survey attracted…

Read More

Accelerated funds availability allows depositors to instantly access the money they deposit via check. That way, there’s no waiting period for the check to clear and no penalty if the check writer’s account has insufficient funds. An article at BAI Banking Strategies by Victoria Dougherty, director of Payment Management Solutions, Fiserv, opens by wondering why…

Read More

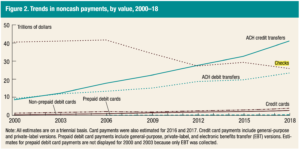

The Federal Reserve released the 2019 Federal Reserve Payments Study Executive Report on December 19, 2019. Based on 2018 compared to 2015, aggregate payment growth in “core noncash payments,” including debit card, credit card, ACH, and checks, were up as a whole by 6.7% representing an incremental 30.6 billion transactions valued at $97B! Comparing actual…

Read More

Real-time payments in the healthcare space, while catching on, are far from ubiquitous at this point. As reported by PYMNTS.com, barriers to real-time payment adoption remain, despite the benefits observed in other consumer-facing industries like insurance and financial services. The costs involved in implementing new services are among the top concerns for payment providers, of…

Read More

We love this time of year! It’s a week when everyone the payments industry can take a deep breath, celebrate successes, reflect, and then blog about the future. And now that 2020 is upon us, what better time to “look ahead” toward 2030! PYMNTS.com is one of the first publications to make a prediction related…

Read More

And another year comes to a close! It’s been our pleasure to share observations, insights, and solutions from across the industry via the OrboNation Blog. As 2019 comes to end, we have much to be thankful for. Most importantly, however, we’re thankful for the clients and customers that are crucial to OrboGraph’s success. Looking back,…

Read More

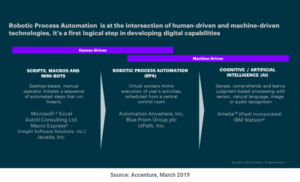

As part of a recent series of blog posts about Intelligent Automation, Adam Swinglehurst of Accenture offered the chart below to illustrate the necessary “overlap” as AI solutions develop and improve. The role of intelligent automation is important to Chief Financial Officers (CFOs) across the globe. CFOs seek to drive efficiencies, create team capacity, meet…

Read More

Last month, the consulting company Navigant published insights titled “5 Pain Points for Revenue Cycle Executives”, based on a survey of Hospital Revenue Cycle Executives conducted in partnership with the Healthcare Financial Management Association (HFMA) and prepared by professionals with direct experience working with healthcare professionals in executive and revenue cycle leadership. As reported via…

Read More

This summer, price transparency advocates finally made progress with a new executive order on “Improving Price and Quality Transparency in American Healthcare to Put Patients First”. In a RevCycleIntelligence article, several hospitals warned that prices may actually increase with such an order — not surprising, in that reforms many times have unknown ramifications due to…

Read More